Ever needed a financial safety net? A line of credit can be just that. It’s basically an agreement where a bank or financial institution allows you to borrow money up to a certain limit, and you only pay interest on the amount you actually use. It’s different from a traditional loan where you borrow a fixed amount and pay it back in installments. Think of it like a credit card, but potentially with better terms and larger credit limits.

Imagine you’re a small business owner and you suddenly need to cover unexpected expenses, or you want to seize an opportunity to invest in new equipment. A line of credit can provide you with the funds you need quickly and easily, without having to go through the lengthy process of applying for a loan each time. It offers flexibility and peace of mind, knowing that you have access to funds when you need them.

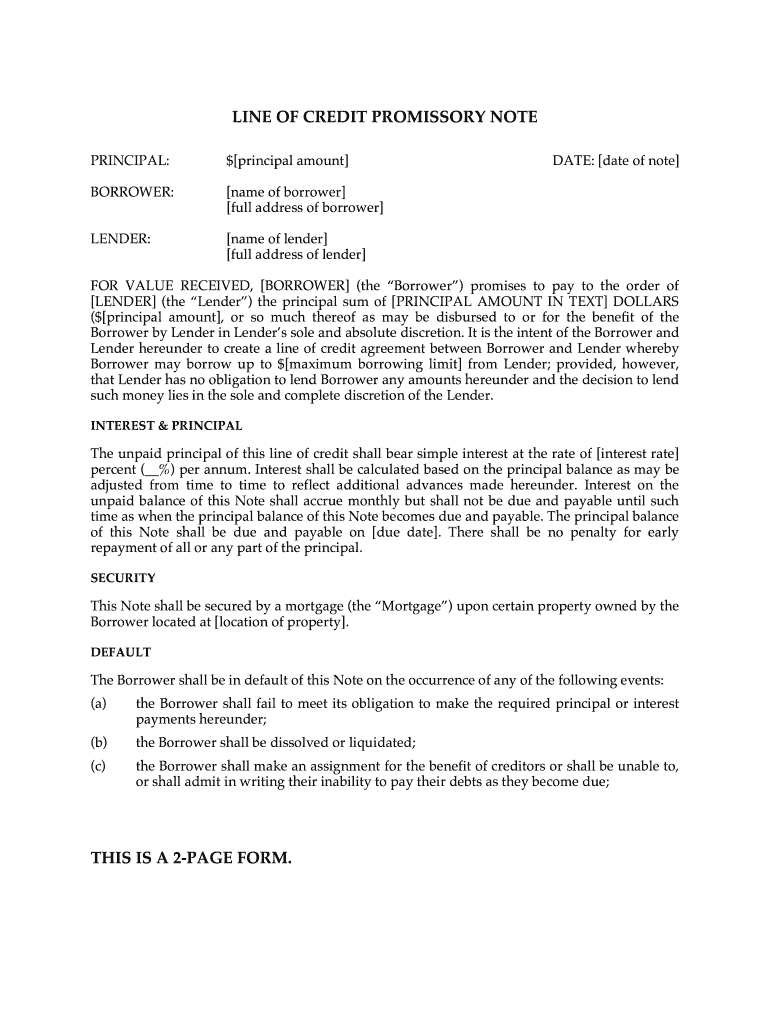

Crafting a solid line of credit agreement is essential to ensure both the lender and the borrower are protected. This is where a well-defined document comes into play, clearly outlining the terms and conditions of the credit line. Think of it as the rulebook for how the credit line will operate, minimizing potential misunderstandings and ensuring a smooth borrowing experience.

Understanding the Essentials of a Line of Credit Agreement

A line of credit agreement is more than just a piece of paper; it’s the foundation of a financial relationship. It details everything from the amount of credit available to the repayment schedule and what happens if things go south. Having a clear and comprehensive agreement is crucial for both the lender and the borrower, setting expectations and preventing future disputes. A strong agreement builds trust and provides a framework for a successful financial arrangement.

The agreement should clearly state the credit limit, which is the maximum amount of money the borrower can access. It will also specify the interest rate, whether it’s fixed or variable, and how it’s calculated. This is crucial for the borrower to understand the cost of borrowing and plan their finances accordingly. Furthermore, the agreement will outline the repayment terms, including the minimum payment amount and the due date.

Beyond the basics, the agreement should address potential scenarios, such as late payment fees, over-limit charges, and the lender’s right to terminate the agreement. It should also include provisions for collateral, if any, securing the line of credit. This could be assets like real estate or equipment that the lender can seize if the borrower defaults on the loan.

The importance of seeking legal counsel when establishing a line of credit agreement cannot be overstated. An attorney can review the agreement, explain complex legal terms, and ensure that your interests are protected. Whether you’re a lender or a borrower, having an expert on your side can provide valuable guidance and peace of mind.

When creating a line of credit agreement template, remember to include sections that clearly define the parties involved, specify the governing law, and outline the dispute resolution process. A well-drafted agreement will not only protect your financial interests but also foster a positive and transparent relationship between the lender and the borrower. If you want to start, using a line of credit agreement template can be a great help to start.

Key Clauses to Include in Your Line of Credit Agreement Template

When drafting a line of credit agreement, it’s important to be thorough and consider all possible scenarios. One critical clause is the “Default” section. This section outlines the events that would trigger a default, such as failure to make payments, breach of any other term in the agreement, or bankruptcy. It should also specify the lender’s remedies in case of default, such as accelerating the debt, seizing collateral, or pursuing legal action.

Another important clause is the “Representations and Warranties” section. In this section, the borrower makes certain promises to the lender, such as that they have the legal capacity to enter into the agreement and that the information they provided is accurate. These representations and warranties give the lender assurance about the borrower’s financial health and intentions.

The “Covenants” section outlines the borrower’s ongoing obligations during the term of the credit line. These might include maintaining certain financial ratios, providing regular financial statements, or not taking on additional debt without the lender’s consent. Covenants are designed to protect the lender’s investment and ensure the borrower remains financially stable.

Furthermore, the agreement should clearly define the procedure for drawing funds from the line of credit. This includes specifying how the borrower must request funds, the minimum amount that can be drawn, and any restrictions on how the funds can be used. Clear procedures ensure a smooth and transparent process for accessing the credit line.

Finally, the agreement should include a “Governing Law” clause, which specifies the state or jurisdiction whose laws will govern the interpretation and enforcement of the agreement. This is important in case of disputes, as it determines which legal system will be used to resolve the issue. Including all of these essential clauses in your line of credit agreement template will help create a comprehensive and legally sound document.

Navigating the world of finance doesn’t have to be daunting. With a clear understanding of agreements and a well-prepared template, you can confidently enter into financial arrangements that benefit both parties involved. Remember to always seek professional advice when dealing with complex financial documents.

A strong financial foundation is built on trust and transparency. By creating clear and comprehensive agreements, we can foster stronger relationships and ensure a smoother path to financial success for everyone involved.